Crypto markets can be confusing for new comers. There’s lots of new terminology to learn: blockchain, decentralization, DeFi. And as the industry continues to grow, we can expect to see more new words and phrases being added to our vocabulary.

But what is DeFi? And what does it have to do with blockchain and crypto? Well, let us answer those important questions for you as we take a deep look at what DeFi is all about.

What is Decentralized Finance (DeFi)?

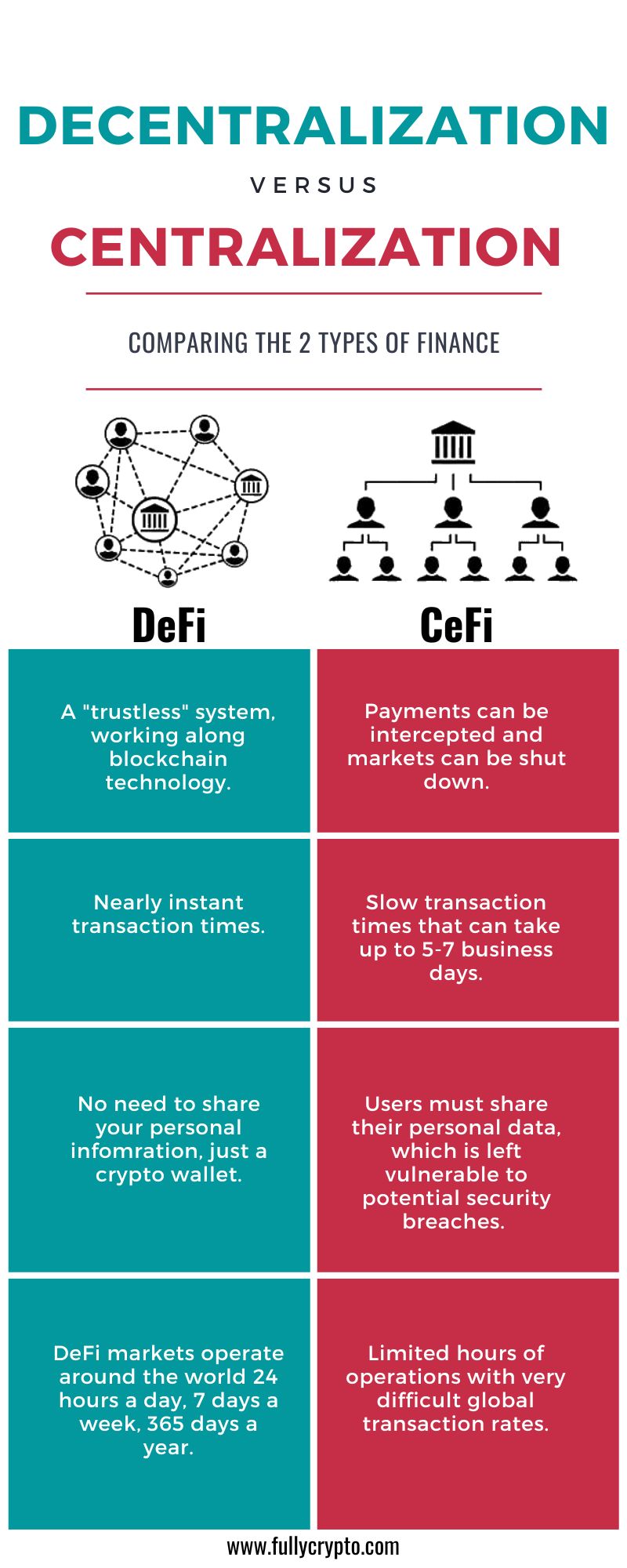

DeFi, or decentralized finance, refers to digital assets and financial smart contracts, protocols, and decentralized applications (dApps) built on decentralized blockchains, such as Ethereum. DeFi aims to create a financial system that is open to everyone and minimizes the need for individuals to trust and rely on central authorities, one of the central tenets of blockchain technology. In short, DeFi allows anyone to take part in a global financial system and look after their own financial affairs without the need for a bank.

DeFi can be beneficial to millions of people across the globe! A decentralized, open-to-all financial system allows those who cannot open bank accounts for whatever reason access to a global financial market, something that has potentially huge implications for countries where individuals or groups of people are restricted from accessing their money by banks or governments.

What is a DAO?

DAO stands for decentralized autonomous organization, essentially an entity with no central leadership. Instead, it is governed by community rule and all decisions are made from the bottom up. To put it simply, anyone who holds any amount of tokens can propose potential changes. Once the suggestion has been made, the community will vote on the proposal where majority rules.

DeFi uses DAOs to allow dApps to become fully decentralized. Since 2020, DOAs have increasingly become the primary DeFi governance mediums in crypto. One of the most important DAOs is Uniswap, largest decentralized exchange on the Ethereum blockchain. UNI holders vote on everything from the protocol’s direction, fees, treasury and more.

DeFi vs. CeFi

How Does DeFi Work?

DeFi apps and protocols are created on decentralized blockchain platforms, typically Ethereum, which use smart contracts to automatically carry out instructions. This ensures that no single entity is in control of the money that is being held or transacted through the app – the application merely facilitates the transaction, and all the funds are held by the user on their device.

This is different to your centralized bank account, where the bank holds your money and you give it instructions of what to do with it. The big difference is that your centralized bank can say no to your instructions if it wants to, or can block you off from your funds entirely if it, or the government of your country, decides it has reason to do so. DeFi apps allow you to act as your bank, meaning you are 100% responsible for your actions.

Decentralized Exchanges (DEXs)

Decentralized exchanges, or DEXs, are crypto exchangeswhere traders make all transactions from peer-to-peer, without relinquishing any money management to a centralized authority, middleman, or outside third party. Essentially, DEXs are vital for the crypto sphere to truly transform into a trustless, P2P means of exchanging value.

Today, centralized crypto exchanges (CEXs), such as Binance, Gemini, Coinbase, Kraken control more than 99% of the cryptocurrency trading market. Estimates released by The Block shows CEXs processed around $14 trillion in volume last year, with DEXs transacting only $1 trillion.

How to Use a DeFi

DeFi exists on networks like Ethereum, Binance Smart Chain, and Polygon, which are all accessible through crypto wallet extensions. These extensions allow users to access their crypto funds directly via their web browsers.

MetaMask is a popular extension you can easily add to your browser which works to “inject the Ethereum web3 API into every website’s javascript context, so that dApps can read from the blockchain.” The extension will also help warn you off sites known for phishing scams. You can also download mobile app versions of these crypto wallet extensions.

You will need to already be in possession of crypto tokens (ETH, BNB, etc.) in order to access DeFi applications. Every transaction you do will need to be manually approved and you will incur a transaction fee.

Once you have successfully attached your crypto wallet to a DeFi application, there’s a number of ways to use the DeFi network.

Lending Platforms

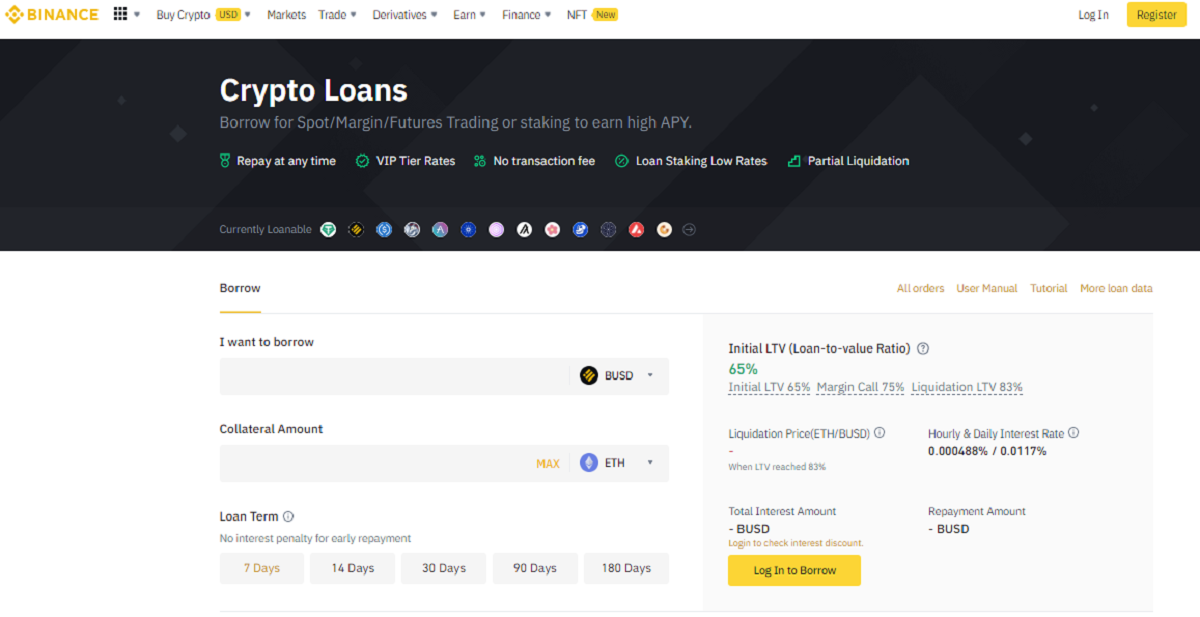

One of the most popular ways to use the DeFi network is for borrowing and lending purposes, known as crypto loans. On these platforms, you can use your crypto as collateral. Interest rates on these loans typically come with interest rates ranging between 1-20% APY/APR. What is unique about crypto loans is that smart contracts automate the process of lending. When taking out a loan on DeFi, you maintain total control of your crypto throughout the entire loan process.

Recently, Binance rolled our their crypto loan program known as Binance Lending. Binance Lending’s periods are short, and those that are happy to deposit a large amount on a regular basis will see a very healthy return over the year. Interest rates very depending on the type of coin with some going as high as 15%.

The Role of Stablecoins in Crypto Loans

Stablecoins are essential to the success of crypto loans as they work to ensure continued stability to DeFi since most, like USDT, are directly tied to fiat currency and are, therefore, much less volatile than other crypto. This stablization through stabelcoins is what allows DeFi to operate as a financial system. This system also allows investors to generate annual yield on their assets.

NFTs

DeFi also has an opportunity for growth through up and coming niches within the crypto market. One such chance is in non-fungible tokens (NFTs). NFTs are cryptographic tokens that can be used to represent real-world assets such as real estate, stocks, and art. The most common types of NFTs range from video game items, original art, memes, and even digital fashion.

Though NFTs are still a relatively new concept and demand has dropped, many market anaylsysts are still predicting that the industry will see a huge influx of private investors and creators over the next five years. The NFT market is currently valued at $40 billion, and most investors believe that they will see huge returns on their investments as the Metaverse expands.

Crypto Debit Cards

A crypto debit card works like your bank card, but is tied directly to your crypto wallet. The only difference here is that it converts your crypto into fiat money. To do this, most crypto debit cards will need to convert your crypto into a stablecoin through the DeFi network and then convert it into fiat currency. You can use your crypto debit card to make transactional purchases and at crypto ATMs.

Popular crypto debit cards include:

Decentralized Insurance Platforms

Like all financial institutions during this digital age, DeFi has seen incidents of exploitation from hackers, a big reason why we are seeing financial regulators call on government intervention on stablecoins. To cover the risks tied to these platforms, you’ll find policies available for dencentralized insurance.

Rather than getting insurance from one specific company, dencentralized insurance is essentially a “pool of providers” who work as the insurance provider by locking up all crypto capital in a dencentralized pool. The pool makes all decisions relating to the insurance platform, including voting on all claims and modifications to the protocol.

Should I Invest in DeFi?

The attraction to DeFi is a combination of technical development, FOMO (fear of missing out), and the growth prospects that the market offers. As the market grows into areas as diverse as asset tokenization, DeFi projects are likely to keep drawing in more investors’ long term.

The average crypto investor is not well-versed on the technical aspects of blockchain technology, and mostly follow gains. Crypto investors follow the money, and DeFi offers a fantastic option both for gains and recovery. Gains, in the sense that the Bull Run of 2021 opened people’s eyes to the limitless potential of blockchain investments. With DeFi projects showing potential for profits, investors have jumped in to try and catch the new wave of growth.

On recovery, lots of investors burned their fingers after the market crash of early 2022. But the market is already seeing restablization and returns. More new ideas continue to emerge, and investors and analysts are excited about the future prospects of all areas of cryptocurrency.

What Are the Risks to Using DeFi?

The lack of a central authority means that, should something go wrong, you have very little means of rectifying it. For example, if someone manages to hack into your app or attacks the blockchain on which it sits, you will be out of luck. Of course, you can report certain actions to the police, and you might get lucky. But the chances of this are remote, given that crypto thieves are adept at covering their tracks.

Also, there is the problem of criminals using DeFi platforms for nefarious activities, knowing that they can’t be watched. The lack of a centralized actor means it’s solely up to police forces to prevent such activities from happening. And while there are ways to reveal the entire blockchain to authorities, criminals rarely use the same address twice, making it difficult to catch them.The FBI has recently even gone so far as to state that cryptocurrencies were a “significant issue” that were only going to get “bigger”.

Why We Need DeFi

The DeFi ecosystem is one of the most vital aspects of blockchain technology. That’s because it provides an avenue for banking the unbanked. There are billions of unbanked people in this world and once fully developed, DeFi will unlock financial solutions in an unprecedented way.

According to internet entrepreneur, and CEO of Civic, Vinny Lingham,

“The reality that we face with this situation, the narrative for many years, has been to open accessibility to more people to use financial services. But the existing banking paradigm has a bunch of risks, costs and consequences, as well as censorship globally, which make it really difficult to scale. For example, if we look at interest rates, look at the difference between what you are receiving and what you are paying, and the profits the banks make. If we think about the way we consider banking, it’s really centralized by nature. You go to a bank, you put money there, they lend it out, and you receive interest. Financial services are broadly someone looking after your money, and they are taking a cut.”

The large unbanked population globally provides an opportunity for long-term DeFi growth and will see the market keep drawing in money over the long term.

FAQ:

- What is DeFi?

The term DeFi stands for “decentralized finance.” These platforms allow users to lend, borrow, and trade cryptocurrencies without a centralized bank or third party entity.

- Is Ethereum a DeFi?

DeFi runs on decentralized blockchains like Ethereum. This creates a financial institution that is open to everyone and minimizes the need for individuals to trust and rely on central authorities

- What is the difference between DeFi and crypto?

Crypto is a form of currency that allows one to partake in a transaction. DeFi is a decentralized financial system that allows crypto investors to lend, borrow, and trade their digital assets.